(Sub-decree No. 48 SD.Prk, dated 11 March 2024)

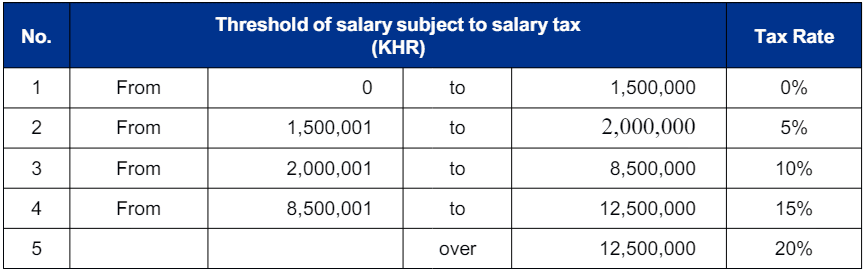

This Sub-decree is issued by the Royal Government of Cambodia (RGC) to determine the threshold of monthly taxable salary of resident employees subject to ToS and the threshold of annual taxable income realized by sole proprietorship and distributions to each member of a partnership subject to annual tax, which shall be effective from 11 March 2024. The threshold of monthly taxable salary of resident employees subject to ToS are as follows:

For resident employees, the tax relief for the spouse and for each dependent child amounting to KHR150,000 per person per month shall be deducted from the gross salary of the employee to arrive at the taxable salary base. In cases where both spouses are employed, the tax relief shall be applied to only one spouse. The threshold of annual income subject to annual tax (i.e., for a sole proprietorship and income distributed to each member of a partnership that is not considered a legal person) are as follows:

Source: KPMG

If our sharing this article infringes on your company's intellectual property, please contact us at info@royalcta.com.kh so that our team will remove this article. Our purpose is just participating and share the update information to the public and taxpayers to be more understood and participate to do compliance in tax and other legal obligation. Thank you!